The Economics of Sustainability-linked Bonds

Researchers from the Geneva Finance Research Institute (GFRI) at the University of Geneva Tony Berrada, Leonie Engelhardt, Rajna Gibson and Philipp Krueger recently wrote a paper on the economics of sustainability-linked bonds, a novel type of sustainability related fixed-income instrument. This new analysis could guide policy-makers by identifying when and under what conditions this sustainability instrument is effective.

In the paper “The Economics of Sustainability Linked Bonds” the authors develop a conceptual framework to analyze the incentive structure and pricing of Sustainability-Linked-Bonds (SLBs), a novel type of sustainability related fixed-income instrument that has emerged as an attractive alternative to Green Bonds from which it differs in important ways. The main particularities of SLBs are that they are not bound to green or environmentally related projects but can be used by the issuer for all types of expenses. The coupon payment structure of these bonds depends on the achievement of a predefined sustainability target at a pre-specified date, and a penalty is typically added to the coupon if a target based on a measurable sustainability Key Performance Indicator (KPI) is not met. Finally, the sustainability target is not limited to environmental issues but can also cover social and governance aspects such as gender diversity, workplace safety, and human rights, among others.

This research addresses two main questions:

– When and under what conditions are SLBs effective in inducing managers to exercise the necessary effort to meet the predefined sustainability target at the pre-specified date?

– How well does the market price these instruments?

To address these questions, the writers developed a model and a mispricing measure that captures whether an SLB is fairly priced. The mispricing measure relies on an SLB’s actual issue price and an upper and lower bound defined respectively as the theoretical SLB prices if the sustainability target is reached for sure and if it is never reached. This procedure allows to circumvent the fact that we can neither observe the probability of a firm reaching the target nor the sustainability appetite and thus the demand of investors for a specific SLB issue. Moreover, with themispricingmeasurewe can identify the extent of mispricing for each individual bond as well as potential wealth transfers between bond- and shareholders at issuance.

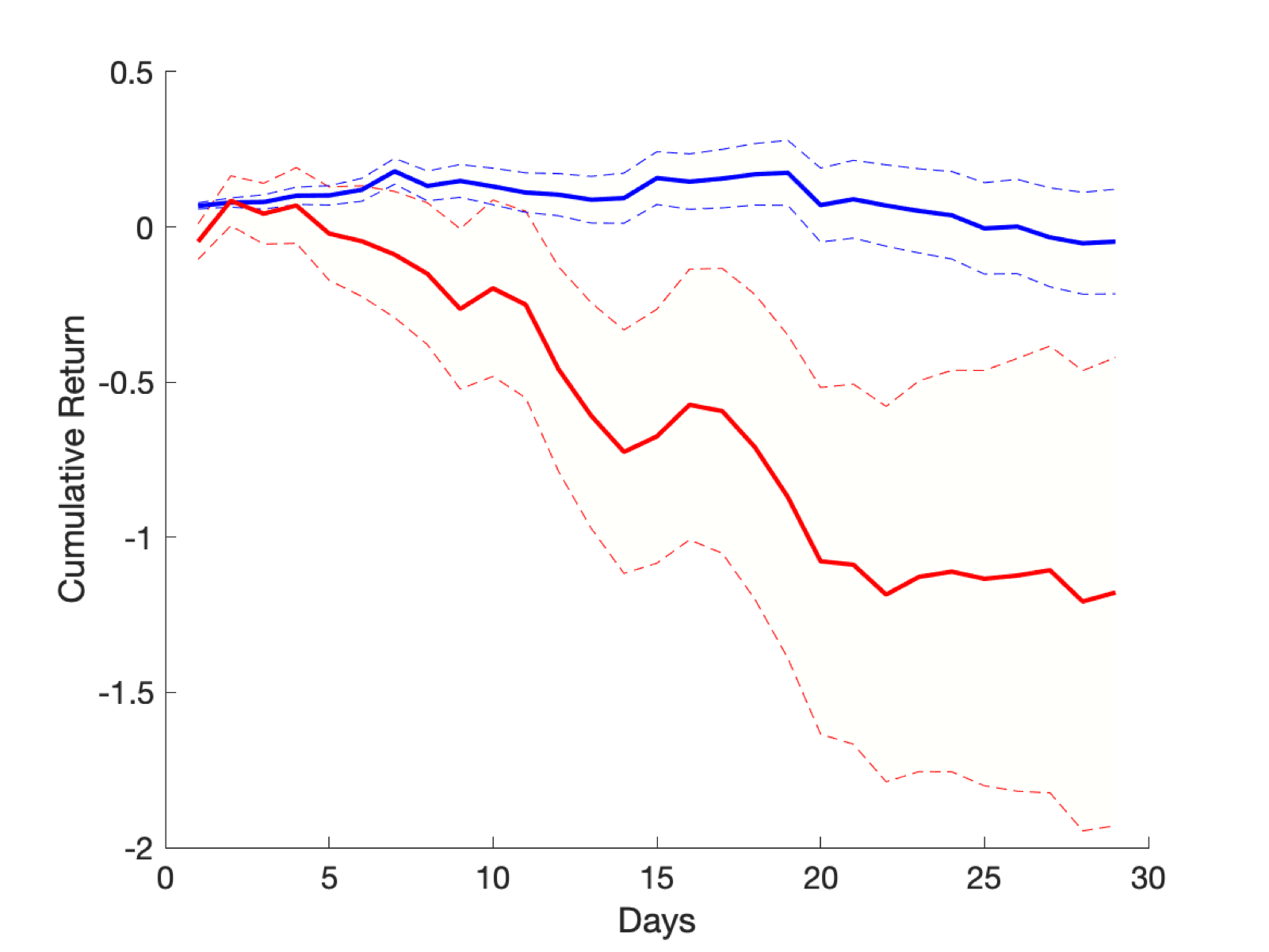

Three main findings can be driven from their empirical analysis. First, SLBs seem to provide proper incentives for borrowers and work as an effective means to achieve desirable sustainability goals at the firm level provided that the penalty in case of failure is sufficiently high. Second, when the mispricing measure is strictly larger than one, SLB issues are overpriced. The overpriced bonds represent about 20 % of the sample. Empirically, such overpricing leads to a post-issuance decrease in their prices on the secondary bond market (see figure below). The secondary market performance difference between overpriced and underpriced bonds is about 1 percentage point during a 30-day horizon after issuance. In the figure below, the solid red (blue) line shows the 30-day post-issuance cumulative returns of overpriced (underpriced) SLBs.

The second finding is that when firms issue overpriced SLBs, a significant wealth transfer occurs from the bondholders to the shareholders of the issuing firms: stock prices react more positively when firms issue more overpriced SLBs. Indeed, a 1.8 percentage points higher abnormal stock market reaction can be observed for an interquartile range increase in themispricing measure. Third, there is large heterogeneity in the pricing (and resulting yield discounts or premiums) of these bonds. The authors also document a statistically significant though complex and non-linear relationship between the mispricing measure and the issuing firm’s ESG rating.

A final and important practical implication of the analysis is that it allows to compare the original market yield of each SLB at issuance with the standard industry computed yield at issuance. This yield comparison suggests that the industry generally overstates the yield discount on an SLB for the issuing firm because the industry yield typically does not consider the expected coupon penalty faced by these firms.

These findings have important implications for policymaking. Policy-makers and financial regulators are well advised to pay special attention to the bond prospectus and certification process as to require firms to disclose the cost of implementing the environmental, social, or governance infrastructure needed to reach their sustainability goals. Furthermore, in the context of an increasing volume and variety of sustainable-related financial instruments where the performance of new securities and infant markets is still not fully observable and understood, promoting sustainable financial literacy among market actors is highly desirable at both the public and private sector levels to improve market pricing and avoid greenwashing problems.

Guest contribution by the SL4SF at the Geneva Graduate Institute

Further information:

Berrada, Tony and Engelhardt, Leonie and Gibson, Rajna and Krueger, Philipp, The Economics of Sustainability Linked Bonds (March 15, 2022). Swiss Finance Institute Research Paper No. 22-26, European Corporate Governance Institute – Finance Working Paper No. 820/2022, Available at SSRN: https://ssrn.com/abstract=4059299 or http://dx.doi.org/10.2139/ssrn.4059299